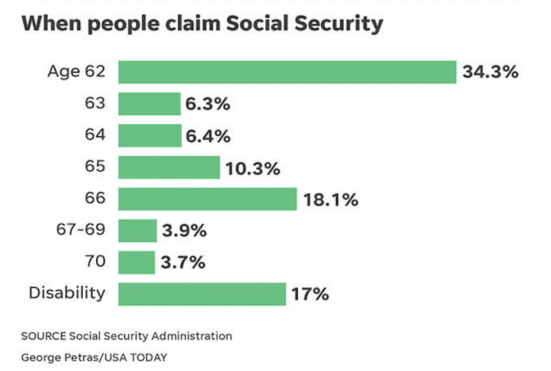

Social security strategy is certainly a “frequently asked question” here at 5280 Associates. It’s no wonder, as this topic affects nearly everyone, particularly those who are nearing retirement age. The most common age for people to claim social security is, by far, age 62 (34.3%) followed by age 66 (18.1%) and age 65 (10.3%). But just because 62 is the earliest you can take social security, doesn’t make it the best strategy for everyone.

Caplinger, Dan. “What’s the most popular way to take Social Security?” The Motley Fool, USA Today content partner. June 19, 2018.

You might think the only decision to make is what age you will start taking your benefits. Not so fast! There are many other factors involved in making smart decisions regarding your social security benefits, and your Financial Planner should be involved to guide you through each one. Read on for some thought starters, and don’t hesitate to give your wealth advisement team a call to discuss how each factor relates to you personally.

Social Security Strategy

Asset Level

Assets are the part of your portfolio that refer to the accounts you have. They may be IRAs, Investment Accounts, Roth IRAs, etc. The unique aspect of assets is that they are typically market based and they can run low or even down to zero! If you have a large sum of assets it may make sense to delay the start of social security because the assets you own can provide income through withdrawals in the early years of retirement. If you do not have sufficient assets you may need to begin social security a little earlier in order to make ends meet. Determining where you fall on the asset scale is relative to the amount of money you plan on spending annually. A detailed, ongoing financial plan is essential to determining your asset level and need for social security benefits.

Other Income Available

Although less common, retirees may have access to a pension. A pension can be defined as a stream of income that usually lasts for your lifetime. A stream of income is very helpful in retirement as an automatic paycheck is deposited into your bank account each month. If you have a significant pension payment, you may be able to delay taking social security as your income need is satisfied. If you do not have additional income available, social security may need to begin earlier to supplement income needs.

Life Expectancy

Social security can be taken anytime between age 62 and 70. The “full retirement age benefit” (FRA) is the full social security benefit as defined by the administration. Most people’s FRA is between ages 66 and 67 depending on the year of birth. If you take social security before FRA, the value is reduced. If you take the benefit after FRA, the value is increased.

For example, a person with a $2,500/month FRA at age 67 who takes social security at age 62 would only get $1,760. Similarly, if the same person took the benefit at age 70, they would get $3,100. So, why wouldn’t everyone take it at age 70? Life expectancy. If you take social security early, and then live a long time, you are forever penalized with the lower amount. However, if you take social security at 62 and die at age 75, you would have gotten more out of the system than if you waited until age 70. For most people there is a breakeven point around age 82 where if you delay until 70 you must live past 82 to get more income from the system than if you decided to take the benefit prior to 70 and died before 82.

Are you married?

A lesser discussed factor in social security decision making is the survivor benefit. When married and one spouse passes away, the higher of the two amounts of social security continues to pay to the

surviving spouse. For example, Ed has a $2,000/month benefit and Mary has a $1,500/month benefit (both receiving the FRA benefit) and Ed dies, Mary will continue to receive an amount equal to $2,000/month total. So married couples should think about coordinating their benefits to maximize one of them if they suspect a longer life expectancy for at least one of the spouses.

Social Security is a vital strategy to incorporate into your retirement plan. Receiving deft advice is crucial, as the recommendations will vary starkly from individual to individual given the factors above, among others. When choosing your Financial Planner, it is very important to ask if they have a social security expert on their team!

As the reliance on the internet continues to grow, so does the need for cybersecurity. According to the cybersecurity company Norton, there are around 2,200 cyberattacks per day. In the ever-changing world that we live in, it is imperative to protect your private...

The holiday season is right around the corner! Donating to an organization can be a great way to spread cheer supporting a cause you believe in while also benefiting from a tax perspective. In this article, we will cover tax implications and strategies around five...

The COVID-19 pandemic was a completely unprecedented event that left our economy at a near-standstill in 2020, causing downward pressure on pricing in many different industries. Now, the economy is beginning to heat back up creating new demands for goods and services...