Investing can be intimidating, even in “normal” times, but throw in one of the most volatile stock markets in US history, and investing can become almost unapproachable for some. As you may know, 2020 has certainly been a roller coaster for the stock market. We have already seen historic market volatility this year and it’s not even halftime yet.

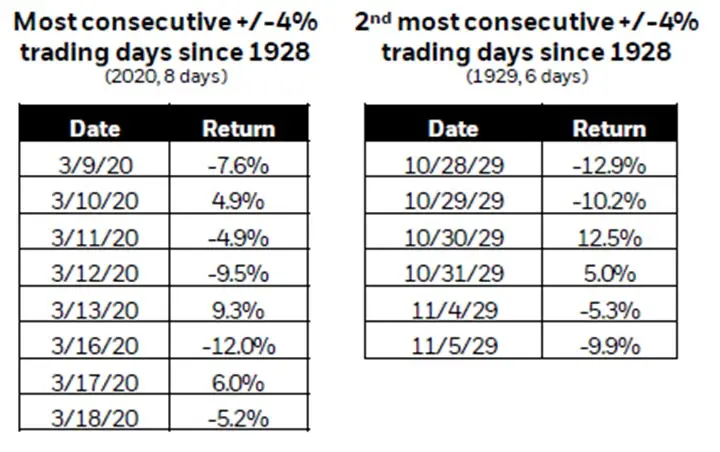

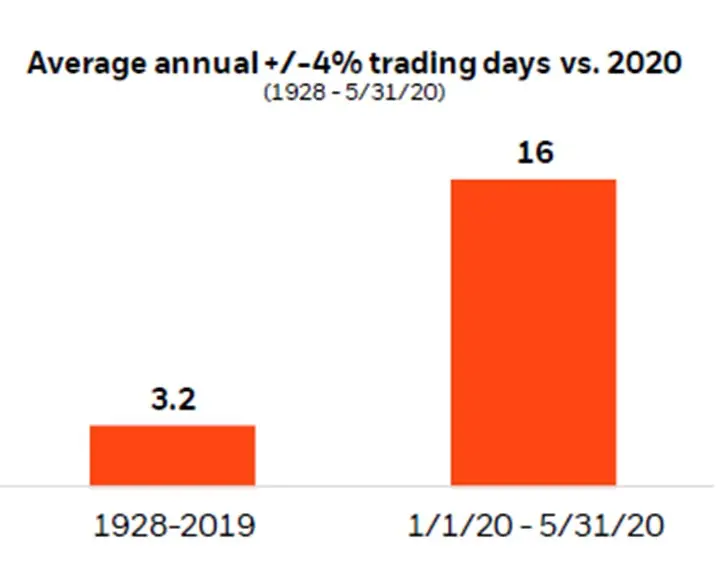

From March 9, 2020 – March 18, 2020 we had 8 consecutive trading days where the S&P 500 traded positive or negative at least 4%. You’d have to look back to the start of the Great Depression in 1929 to find the year in 2nd place for the most consecutive +/ – 4 % trading days. They had 6 that year. Since 1928, on average, the S&P 500 has about 3.2 trading days annually where the index is +/ – 4%. Up to May 31st of this year, we have already had 16.

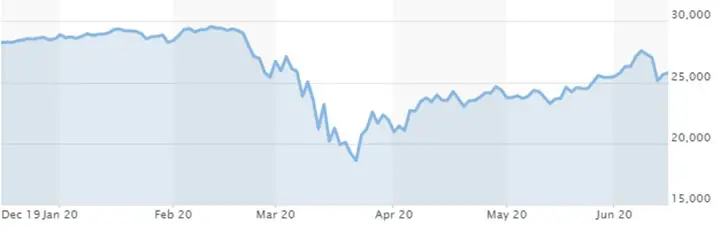

On top of that, we have seen the biggest single day point drop AND the biggest single day point gain for the DOW in market history. As you can see in the chart below, DOW gained 2117.72 points on March 24, 2020 and lost 2997 points on March 16, 2020.

While it’s not ideal to be living through a volatile stock market like this, it’s important to remember that volatility is a part of the investing environment and that long-term investors should not react to day-to-day market fluctuations and attempt to time the market.

Key #1 – Keep your money invested during a Volatile Stock Market

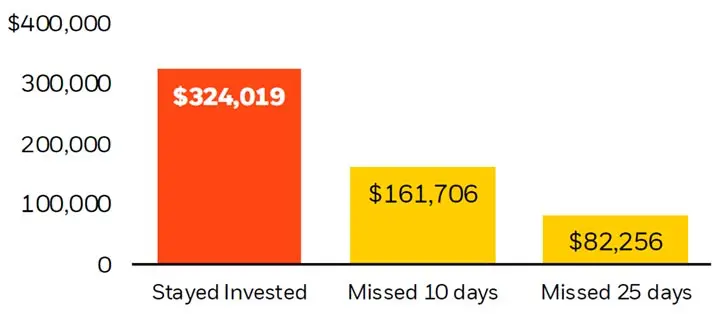

It’s a lot easier said than done for most. Take a look at the hypothetical example below provided from Blackrock to explain the importance of not attempting to time the market.

From January 1, 2000 to December 31, 2019, if you invested $100,000.00 in the S&P 500 Index, your account balance would have grown to $324,019.00. However, if during those 20 years you attempted to buy/sell when the market was up/down and your money was not invested or “missed” the top 10 positive market days, your account only would have grown to $161,706.00. To further illustrate the point, if you missed the top 25 days, your account balance would have declined to $82,256.00. Keep in mind you can’t invest directly in an index.

If you are attempting to time your investments, you are leaving yourself vulnerable to emotions. Market timing is mostly driven by fear of loss. Don’t be your own worst enemy and instead of attempting to time the market, try these steps:

Designate a purpose for each investment account you hold (Why do I have each account?)

Evaluate your time horizon (When are you going to use the funds in each account?)

Assess your diversification strategy (How much risk should you be taking?)

Look for opportunities to rebalance (Have positions drifted from your target allocation?)

Be confident in your plan.

Key #2- Control your emotions during a Volatile Stock Market

There are many risks associated with investing, to give you a few examples: market risk, interest rate risk, liquidity risk, credit risk, inflation risk, concentration risk, and, lastly, because it’s an election year, political risk. The key here is having a basic understanding of the risks associated with your investments and setting clear expectations to help mitigate the danger of emotional investing. That means doing your due diligence and understanding the fundamentals of the company/fund before purchasing. It means being realistic in forecasting returns and projected volatility. It also means being knowledgeable about common emotions and pitfalls that investors experience such as chasing past performance, following the crowd, not having patience, failing to diversify, or waiting to get even. Developing and committing to a long-term investment plan may be the best way to combat these emotions. For long-term investors, reacting emotionally to volatility may be more detrimental to your portfolio than simply letting the market run its course. Taking the time up front to understand your investment and level set expectations can pay off when times of uncertainty kick in.

Key #3 Look for opportunity during volatility

Volatility creates opportunity for many investors. Take a look at some of the concepts in my partner’s recent blog: The Silver Lining of the Coronavirus Impact on Financial Planning. While largely unrelated to this post, some of the concepts in that article are savvy planning techniques to utilize during volatile times. Specifically, Roth conversions and tax loss harvesting are two prime examples of opportunities created by volatility. In both circumstances, you would benefit from selling stocks/funds at a lower share price and realizing less in taxes.

Rebalancing your portfolio during times of volatility can also have a meaningful impact long – term. However, in order to initiate a rebalancing strategy, you need to have a plan up front. What’s the purpose of the account and when you set it up, what percentage did you allocate to equities and/or to Bonds? Current market conditions should not dictate your target asset allocation strategy but rather provide guidance on how to perform the rebalance. Rebalancing simply means adjusting your portfolio back to its original allocation structure.

As a hypothetical example, let’s say your portfolio you set up a year ago has a current allocation of 50% equities and 50% bonds, but you initially set the target allocation for the portfolio of 60% equities and 40% bonds. If you were to rebalance your portfolio now, you would be selling bonds and buying more equities to get back to your target allocation of 60% equities and 40% bonds. Assuming the equity market has declined and the bond market has increased in this example, you benefit from the rebalance due to the fact that you are selling the bond portion of your portfolio at higher prices and purchasing into the equity portion of your portfolio at lower prices.

Key #4 Stick to the Investment Plan

Remember, volatility is a natural part of market cycles, it is unavoidable, yet it presents investors with opportunity. Creating and adhering to a plan helps you avoid making costly mistakes – like trying to time the market or letting your emotions drive actions. Instead, ignore the noise, focus on your goals, and let your game plan create a sense of reassurance while others go into panic mode.

No matter the year, the environment, or the worldwide events, investing can be daunting. By keeping your money in the market, prohibiting emotions from taking the lead, finding opportunities, and sticking to a strict plan, investing can go from unnerving to rewarding during a volatile stock market.

Imagine a retirement where you not only have a reliable income stream but also the satisfaction of knowing you're making a lasting impact on the causes you care about. A charitable remainder trust (CRT) is a tax-efficient donation strategy that might be the tool you...

For high-income earners, tax planning isn’t just about complying with the law—it’s a critical strategy for preserving wealth and minimizing unnecessary liabilities.

Retirement offers the chance to give back in ways that weren’t possible before, and charitable contributions from your IRA provides a smart, efficient way to do so.